Emergencies can strike at any time, and being financially prepared is crucial to ensure your family’s security and peace of mind. Whether it’s a medical crisis, a sudden job loss, or unexpected home repairs, having a solid plan can help you navigate through tough times without added financial stress. As a Licensed Financial Planner, I want to share some essential strategies to help Malaysian families prepare for emergencies effectively.

The Importance of Emergency Planning

Emergencies are unpredictable and can have a significant financial impact. Planning ahead allows you to manage these situations more effectively, reducing stress and ensuring that your family can maintain their standard of living.

Key Components of Emergency Planning:

- Emergency Fund: A dedicated savings fund to cover unexpected expenses.

- Insurance Coverage: Adequate health, life, and property insurance to mitigate financial losses.

- Debt Management: Strategies to manage and reduce debt, providing financial flexibility during emergencies.

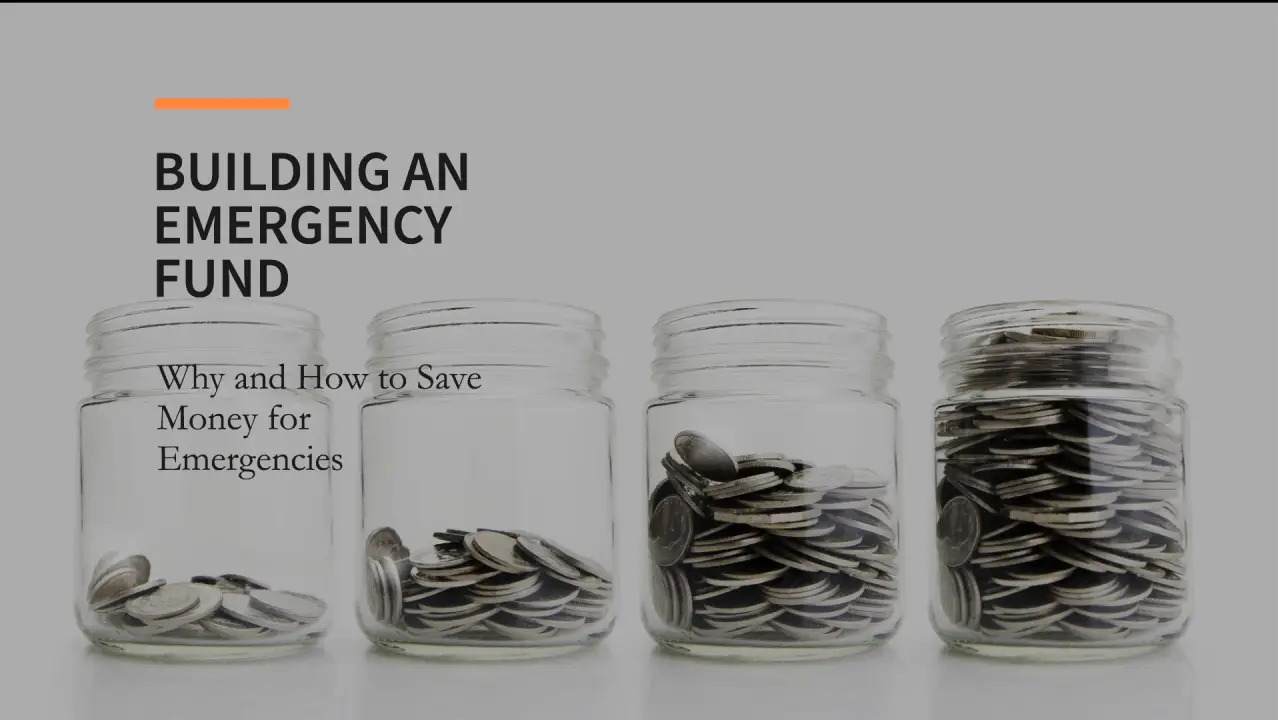

Building an Emergency Fund

An emergency fund is a cornerstone of financial security. It’s essential to have a dedicated fund that you can tap into during unexpected events.

How Much Should You Save?

Financial experts typically recommend saving three to six months’ worth of living expenses. This amount can provide a cushion during emergencies, allowing you time to recover financially without resorting to high-interest debt.

Strategies for Building an Emergency Fund:

- Automate Savings: Set up automatic transfers to your emergency fund to ensure consistent savings.

- Cut Unnecessary Expenses: Identify and reduce non-essential spending to boost your savings rate.

- Increase Income: Consider side gigs or freelance work to accelerate your savings.

Example: By saving RM500 monthly, you can build a RM6,000 emergency fund in just one year, providing a substantial safety net for your family.

Insurance: Your Financial Safety Net

Insurance is a critical component of emergency planning. It provides financial protection against unforeseen events, helping you manage significant expenses without depleting your savings.

Types of Insurance to Consider:

- Health Insurance: Covers medical expenses, ensuring access to quality healthcare without financial strain.

- Life Insurance: Provides financial support to your family in the event of your untimely demise.

- Property Insurance: Protects against damages to your home and personal belongings.

Example: A comprehensive health insurance policy can cover hospital bills and treatment costs, reducing the financial burden during medical emergencies.

Debt Management

Managing debt effectively ensures that you have the financial flexibility to handle emergencies. High-interest debt can be particularly burdensome during crises, so it’s important to have a plan to manage and reduce your debt load.

Strategies for Debt Management:

- Prioritize High-Interest Debt: Focus on paying off high-interest debt first to reduce overall interest payments.

- Debt Consolidation: Consider consolidating multiple debts into a single loan with a lower interest rate.

- Create a Repayment Plan: Develop a structured plan to pay off debt systematically, freeing up resources for emergency savings.

Example: By consolidating credit card debt into a lower-interest personal loan, you can reduce monthly payments and allocate more funds to your emergency savings.

Estate Planning

Estate planning ensures that your assets are managed and distributed according to your wishes, providing financial security for your family even in your absence.

Key Elements of Estate Planning:

- Writing a Will: Clearly outline the distribution of your assets to avoid legal complications.

- Setting Up a Trust: Protects your assets and provides for your family according to your wishes.

- Power of Attorney: Designate someone to make financial and healthcare decisions on your behalf if you’re unable to do so.

Example: Establishing a trust can ensure that your children’s education and living expenses are covered, even if you’re no longer able to provide for them directly.

Conclusion

Planning for family emergencies is a crucial aspect of financial stability. By building an emergency fund, securing adequate insurance coverage, managing debt, and engaging in estate planning, you can ensure that your family is prepared for any eventuality. Remember, the key to successful emergency planning is to start early and stay disciplined.

Sources:

- Bank Negara Malaysia

- Life Insurance Association of Malaysia (LIAM)

- Private Pension Administrator Malaysia (PPA)

Disclaimer: This article reflects my personal views and experiences as a Licensed Financial Planner. It does not represent the opinions or positions of any company or third party. The information provided is for general informational purposes only and should not be considered financial advice. Always consult with a professional like Dr. Rajendaran Vairavan, a Licensed Financial Planner with CFP certification, for your specific financial needs.

Connect with Me

If you found this article helpful, feel free to connect with me on LinkedIn. Let’s grow our financial knowledge together and work towards achieving our financial goals. Share this article with your network to spread the knowledge and encourage more people to start their financial planning journey.